High Frequency Trading

Feature Resampling

Tick data feeds are often aggregated into candlestick bars. Classical candlesticks are sampled with respect to time, but this choice is fairly arbitrary — for one, we know that markets do not trade at a uniform speed (Kyle & Obizhaeva, de Prado). For instance, market open and closing hours tend to be more liquid. Time bars oversample information during periods of low activity, and vice versa. Consequently, time sampling often exhibit poor statistical properties.

Sampling as a function of other variables, such as number of transactions (Mandelbrot, 1963), allows us to achieve samples closer to i.i.d. Gaussian distributions, making them more amenable to statistical modeling and interpretation.

Typical information included in aggregated bars include t (start), open, high, low, close, volume, n (number of ticks), vwap, T (end).

Let \( t_n \) be the current timestamp, then time bars are sampled when \(t_n > T\), where \( T = t + \tau \), a fixed interval length. We shall explore some alternative sampling methods.

- Tick Bars Set a constant tick count \(c\). Roll the bar when: \( n > c \).

- Volume Bars / Dollar Bars Analogous to tick bars, but triggered when total volume or dollar value exceeds a threshold.

Let a trade be defined by its timestamp, price, size, and direction, then

and for some \( \delta \) threshold, the samples are taken when

- Signed Tick Bars:

- Signed Volume Bars:

- Signed Dollar Bars:

Probabilistic Bars

So far, the bars are somewhat static, but we would like to perform sampling with frequency proprotional to the arrival of information. This new paradigm of information sampling works on a dynamic frequency with respect to deviation from some expected thresholds;

Define:

- \( n_{\text{ticks}} \): target number of ticks per bar

- \( \lambda \in [0,1] \): decay factor

Let:

- Tick imbalance:

- Average tick imbalance:

with expected value (exponential online estimate):

Then roll when:

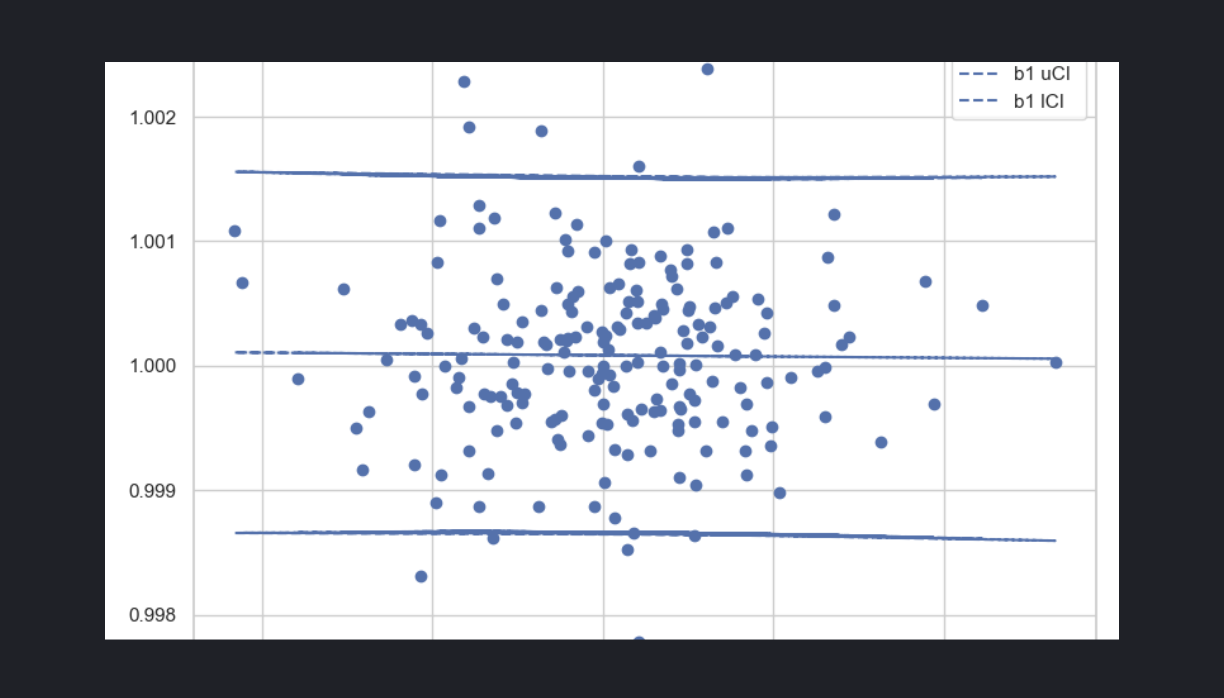

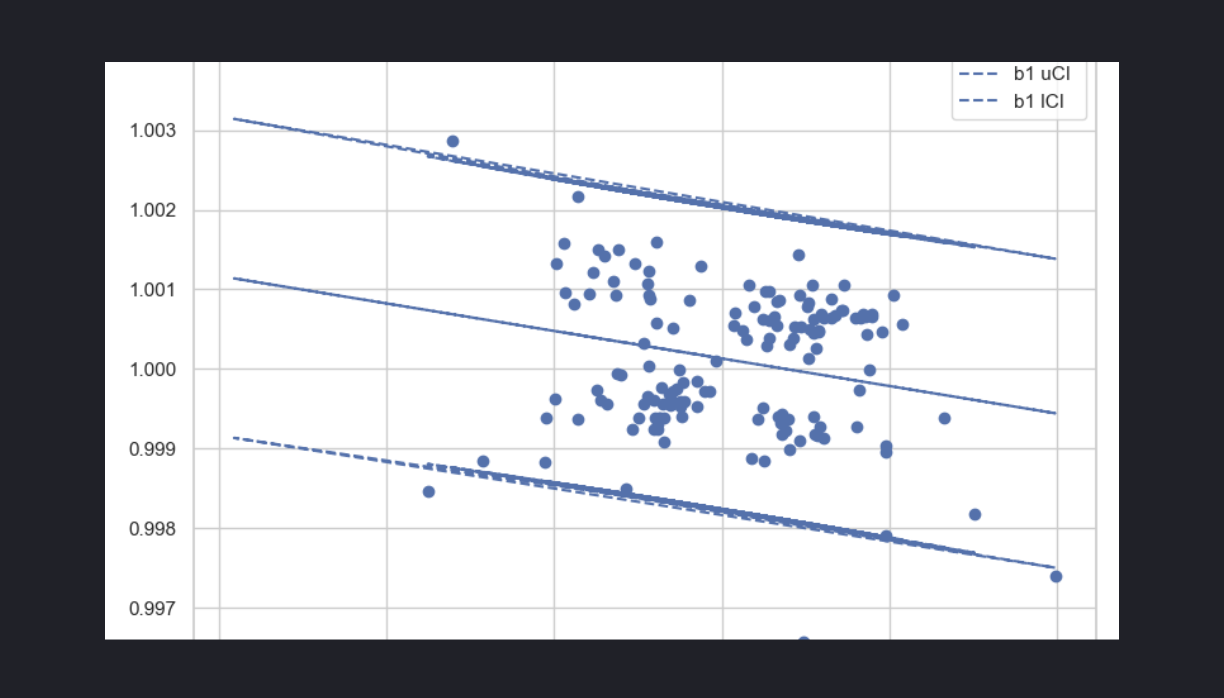

Some Results A small numerical test is proposed to observe if BTC trade ticks exhibit mean-reversionary effects to vwap levels. Volume is often considered to be a metric of informed traders with asymmetric information crossing the bid-ask spread. It is reasonable to suspect that prices with higher volumes act as anchors. We test this relation using a simple regression relationship between time-series bar samples:

The trials are repeated for (i) classical time bars, and (ii) probabilistic bars. Data archival, restoration, tick data replay and regression analysis are all performed using quantpylib's features and Binance websocket data. See tick data management tutorial here. Documentation is here for the hft module. The code for regression trials and subscribing to the custom bar feeds is presented.

Code for Feature Resampling and Regression

import pytz

import json

import asyncio

import matplotlib.pyplot as plt

from datetime import datetime

from dateutil.relativedelta import relativedelta

import quantpylib.hft.bars as bars

from quantpylib.hft.feed import Feed

from quantpylib.gateway.master import Gateway

show = False

exc = 'binance'

tickers = ['BTCUSDT']

stream_data = {

'binance': tickers,

}

run = None

time = None

replayer = None

from quantpylib.hft.mocks import Replayer,Latencies

hours = 10

now = datetime.now(pytz.utc)

start = now - relativedelta(hours=hours)

start = start.strftime('%Y-%m-%d:%H')

end = now.strftime('%Y-%m-%d:%H')

LATENCY = 0

latencies={

Latencies.REQ_PUBLIC:LATENCY,

Latencies.REQ_PRIVATE:LATENCY,

Latencies.ACK_PUBLIC:LATENCY,

Latencies.ACK_PRIVATE:LATENCY,

Latencies.FEED_PUBLIC:LATENCY,

Latencies.FEED_PRIVATE:LATENCY,

}

replayer_configs = {

"latencies":latencies,

}

gateway = Gateway(config_keys={"binance": {}})

async def handler(bar):

print(bar)

async def play_data(replayer,oms,feed,ticker):

trade_feed_id = await feed.add_trades_feed(

exc='binance',

ticker='BTCUSDT',

buffer=100,

)

time_bars = await feed.add_sampling_bars_feed(

exc='binance',

ticker='BTCUSDT',

handler=handler,

buffer=10000,

bar_cls=bars.TimeBars,

granularity='m',

granularity_multiplier=3,

)

probabilistic_bars = await feed.add_sampling_bars_feed(

exc='binance',

ticker='BTCUSDT',

handler=handler,

buffer=10000,

bar_cls=bars.ProbabilisticSignedTickBars,

n_ticks=1500,

)

return time_bars,probabilistic_bars

async def hft(replayer,oms,feed):

bar_feeds = await asyncio.gather(*[

play_data(replayer=replayer,oms=oms,feed=feed,ticker=ticker)

for ticker in tickers

])

await run()

for _type,_bar_feed in zip(['time','probabilistic'],bar_feeds[0]):

bar_feed = feed.get_feed(_bar_feed)

bars = bar_feed.as_df()

from quantpylib.simulator.models import GeneticRegression

configs = {"df":bars}

model = GeneticRegression(

formula="div(forward_1(c),c) ~ div(minus(c,vwap),c)",

df=bars

)

res = model.ols()

model.plot()

print(res.summary())

async def sim_prepare():

trade_data = {exchange:{} for exchange in stream_data}

for exchange,tickers in stream_data.items():

trade_archives = [

Feed.load_trade_archives(

exc=exchange,

ticker=ticker,

start=start,

end=end

) for ticker in tickers

]

trade_data[exchange] = {

ticker:trade_archive

for ticker,trade_archive in zip(tickers,trade_archives)

}

global replayer, run, time

replayer = Replayer(

l2_data={},

trade_data=trade_data,

gateway=gateway,

**replayer_configs

)

oms = replayer.get_oms()

feed = replayer.get_feed()

run = lambda : replayer.play()

time = lambda : replayer.time()

return oms, feed

async def main():

await gateway.init_clients()

oms,feed = await sim_prepare()

await oms.init()

await hft(replayer,oms,feed)

await gateway.cleanup_clients()

if __name__ == '__main__':

asyncio.run(main())

The sampled bars are retrieved as in bar_feed.as_df()

t o h l c v n vwap T

0 1.747516e+12 103330.7 103376.4 103286.5 103286.5 102.308 1389.0 103340.333948 1.747516e+12

1 1.747516e+12 103286.6 103350.0 103248.8 103349.9 93.656 1317.0 103297.011811 1.747516e+12

2 1.747516e+12 103350.0 103458.6 103280.1 103280.1 280.711 2457.0 103403.270401 1.747516e+12

3 1.747516e+12 103280.1 103301.2 103262.4 103301.2 74.626 1001.0 103276.858821 1.747516e+12

4 1.747516e+12 103301.2 103390.2 103301.1 103356.7 105.848 884.0 103353.044096 1.747516e+12

.. ... ... ... ... ... ... ... ... ...

196 1.747551e+12 103417.6 103431.9 103350.4 103359.1 112.305 1143.0 103395.879483 1.747551e+12

197 1.747551e+12 103359.2 103382.8 103350.7 103350.8 57.124 942.0 103366.522973 1.747551e+12

198 1.747551e+12 103350.8 103353.8 103320.0 103353.7 82.479 838.0 103339.882634 1.747551e+12

199 1.747551e+12 103353.7 103386.8 103353.7 103370.6 61.202 714.0 103366.291206 1.747551e+12

200 1.747551e+12 103370.7 103429.4 103353.8 103414.4 144.935 1389.0 103390.268834 1.747552e+12

We obtained the following results for time-based sampling (not significant) and probabilisitic sampling (significant)

OLS Regression Results

==============================================================================

Dep. Variable: b0 R-squared: 0.000

Model: OLS Adj. R-squared: -0.005

Method: Least Squares F-statistic: 0.02410

Date: Tue, 13 May 2025 Prob (F-statistic): 0.877

Time: 21:34:09 Log-Likelihood: 1170.6

No. Observations: 201 AIC: -2337.

Df Residuals: 199 BIC: -2331.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 1.0001 5.08e-05 1.97e+04 0.000 1.000 1.000

b1 -0.0209 0.135 -0.155 0.877 -0.286 0.244

==============================================================================

Omnibus: 11.897 Durbin-Watson: 1.867

Prob(Omnibus): 0.003 Jarque-Bera (JB): 19.713

Skew: 0.315 Prob(JB): 5.24e-05

Kurtosis: 4.399 Cond. No. 2.65e+03

==============================================================================

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

OLS Regression Results

==============================================================================

Dep. Variable: b0 R-squared: 0.059

Model: OLS Adj. R-squared: 0.053

Method: Least Squares F-statistic: 9.050

Date: Tue, 13 May 2025 Prob (F-statistic): 0.00310

Time: 21:34:28 Log-Likelihood: 809.41

No. Observations: 146 AIC: -1615.

Df Residuals: 144 BIC: -1609.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 1.0001 7.89e-05 1.27e+04 0.000 1.000 1.000

b1 -0.3461 0.115 -3.008 0.003 -0.573 -0.119

==============================================================================

Omnibus: 3.589 Durbin-Watson: 2.021

Prob(Omnibus): 0.166 Jarque-Bera (JB): 3.380

Skew: -0.215 Prob(JB): 0.184

Kurtosis: 3.608 Cond. No. 1.46e+03

==============================================================================

Clearly, the numerical experiments reveal some interesting dynamics between sampling behaviour and the presence of mean-reversion effects. Not as clearly, it is important to keep in mind these are time-varying effects, and most perhaps regime dependent.